Good Morning.

First to pass along this link for Crosstex Energy (XTXI) as Raymond James; my guess is on Wednesday, lowered its EPS on XTXI but maintained its outperform rating. Meanwhile the stock is bid above the close in the pre-market today which usually happens with news or an upgrade...but i don't see anything on the news wire. Meanwhile they were more encouraging with Crosstex LP and maintained its eps and targets but enccouaged accumulation on weakness..this was the reverse of what RBC Capital markets did earlier this week.

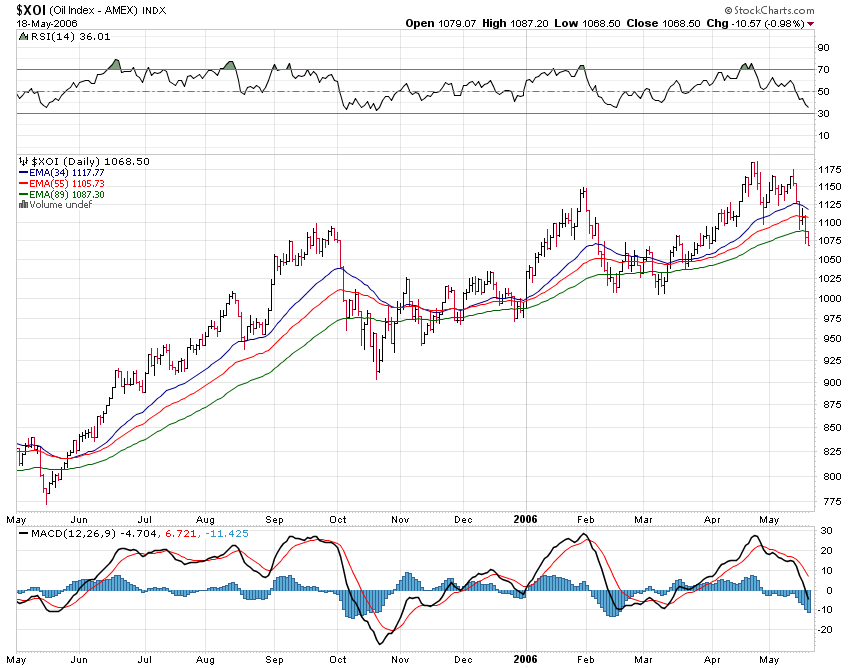

Meanwhile another bounce at the start like yesterday which i don't like in this enviornment...better to have sharp selloffs early and a rally late then the other way around like yesterday. Still MLPS held up nicely yesterday. There is no news in the group this morning. Dow chart and XOI chart above would suggest pressure in the overall market so some of that could spill over into MLPS...but at some point they will act defensive with their supportive yields and should hold or at worst go down less than everything else.

Joe,

ReplyDeleteHere's the RAYMOND JAMES piece from the XTEX message board:

here's an excerpt from a note Raymond James put out today. They have an Outperform rating on both XTEX and XTXI.

>>>>>>>>>>>>>

Wednesday morning, Crosstex announced that it will issue

approximately 12.8 million senior subordinated units for a total of

$360 million (~$28.125 per unit) related to the $480 million

acquisition of Chief Holdings' midstream assets and other organic

growth projects (~$600 million in capital projects over the next few

years).

♦ The sub units will convert to common on February 16, 2008 and will

not be counted in the partnership's distributions or for the calculation

of the general partner's incentive distribution rights until that time.

♦ We are adjusting our 2006 and 2007 EPU estimates to reflect the

higher-than-expected number of units issued (we initially expected

7.5 million units for $240 million). We are raising our 2006/2007

EPU estimates from $(0.21) and $(0.34) to $(0.17) and $(0.16),

respectively. Our EBITDA and distribution estimates for both 2006

and 2007 remain unchanged.

♦ We expect higher distribution coverage levels for both 2006 and

2007 due to the higher number of subordinated units issued (which

do not receive distributions until 2008). Previously, we expected

common equity issuances to finance the North LIG, South LIG, and

Parker County expansion projects (total cap ex of ~$450 mm), but it

appears that this offering will take care of substantially all of the

equity needs for those projects. We expect the remainder of the

capital expenditures to be financed through debt.

♦ Overall, we are maintaining our Outperform rating and our 12-

month price target of $42.00. We encourage investors to buy on the

recent weakness.

thanks carlos..i picked up crosstex at the open friday at 34.13..and some more near the close at 34.82

ReplyDelete