Brokerage houses are on the horn in force this morning as a host of new coverage and upgrades and one or 2 downgrades of note. But overall the houses seem to be falling all over themselves as they talk up MLPS ahead of earnings. Lets start with MLP granddaddy Kinder Morgan Partners(KMP) which gets an upgrade from Wachovia to outperform from market perform and Credit Suisse starts at an outperform with a $54 target. This btw is being done ahead of earnings which are due out after the close today with a conference call to follow. Credit Suisse starts Enbridge Partners (EEP) with an outperform and a $56 dollar price target. organ Stanley starts Energy Transfer Partners (ETP) at overweight. Morgan Stanley and Credit Suisse both start Holly Energy Partners (HEP) at equal weight and neutral respectively.Moving down the list Credit Suisse also starts Plains All American (PAA) at a neutral. Morgan Stanley starts Regency Partners (RGNC) at an outperform. And finally Credit Suisse starts Valero LP at an outperform and puts a nice $62 price target.

We have 2 downgrades of note. Oneok LP is downgraded to market perform from outperform by Wachovia and they also downgrade Crosstex Energy (XTXI) to market perform from outperform. Both of these stocks have been leaders in the group.

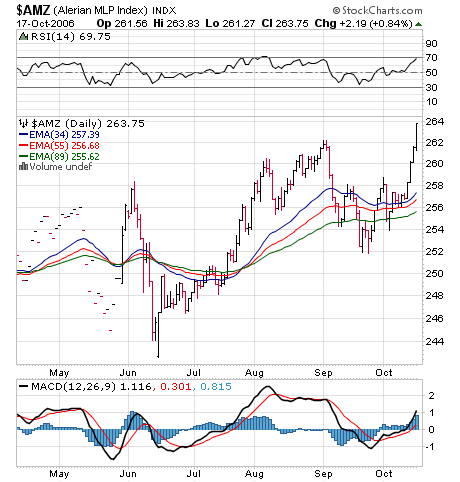

The MLP Index looks like should continue to extend its gains as we brokeout above 262 yesterday in very impressive fashion finishing at the highs of the day. I had predicted weeks ago that we should challenge the 270 weekly top for a decisive breakout above that to new all-time highs. I still stand by that prediction. CPI due out at any moment which will set the tone today with 10 year rates. As long as it behaves get set for some nice upside...and its out and in line with estimates..0.2% up...headline down 0.5%. Its off to the races!

joseph cioffi's Source Page - Associated Content

joseph cioffi's Source Page - Associated Content

4 comments:

Are these the first MLPs that Stanley has covered? I haven't seen their ratings before. That would be great if we have more analysts covering the sector to get it on institutions radar screens.

I guess it depends on your perspective. I am building substantial long-term hold positions in many of these companies and would prefer if the prices stayed low or even retreated for a while. I'd like to keep them off the radar screens of big money for now!

I think this is indeed new for MS although their coverage outperform on RGNC did little to the price by days end. In fact Valero LP gets an outperform by credit suisse and closes up 16 cents after being down most of the day. Oneok LP gets downgraded by Wachovia and the stock was up 64 cents and at another all time high. Go figure.

In the long run these upgrades are good for one day pops if that.

Meanwhile Copano increases its distribution to 75 cents...3 bucks annual. 60 dollar stock price?

Then we agree to disagree. I will cheer for higher prices and you can cheer for lower ;)

KMP flat div and CPNO up 11%. That really says it all. The small natural gas partnerships are still cheap as chips. Of the large MLP's, ETP/ETE is the only one that makes sense to be buying I think. ETE offers the best risk/reward of all in my opinion.

Post a Comment